Hotline

02373 900 333

NEWS

Updated: 04-07-2019 | Views: 1350

Thursday, 04 Month 07 Year 2019 | Views: 1350

PVS forecasted to exceed the profit plan of 2019

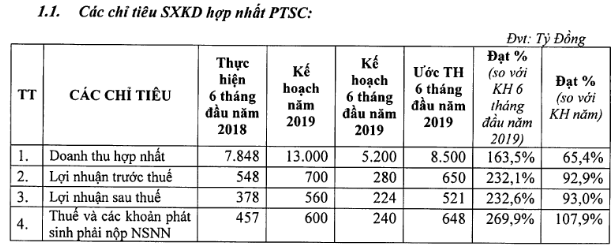

In the first 6 months, PVS is estimated to achieve consolidated profit before tax of VND 650 billion, equivalent to approximately 93% of the annual plan. According to VCSC's assessment, the potential of unearned revenue (backlog) of PVS may increase by about USD 500 million thanks to some signed contracts related to Long Son Petrochemical project and Salman project (Brunei).

According to preliminary report of the first 6 months business results of PetroVietnam Technical Services Corporation (PVS), the consolidated revenue in the first 6 months is estimated at VND 8,500 billion, equivalent to 65.4% of the year plan and profit pre-tax profit of VND 650 billion, reaching approximately 93% of the annual plan.

PVS completed 93% the profit plan after 6 months.

Viet Capital Securities (VCSC) analyzed that the positive results of PVS in the first half of 2019 is based on (1) FSO Ruby II profit increase, (2) Mechanical field got high results due to Sao Vang – Dai Nguyet and Gallaf, and (3) Geological Survey reduce losses after dissolution in late 2018.

VCSC evaluated oil and gas mechanical segment will have a bright prospect in 2019 by (1) PVS has signed a petroleum engineering contract related to Long Son Petrochemical Complex with a total value of USD 100 million and there may be additional contracts signed with this complex; (2) PVS is confident in Salman project in Brunei; (3) Management aims to build contracts for LNG Van Phong Port project (total investment value of about 700 million USD); (4) PVS is currently conducting some initial survey services for ExxonMobil for Blue Whale project (total investment of 10 billion USD).

According to VCSC's assessment, the potential of unearned revenue (backlog) of PVS may increase by about USD 500 million thanks to some signed contracts related to Long Son Petrochemical project and Salman project (Brunei).

PVS bought a tanker and will convert this vessel into FSO to ensure the Sao Vang - Dai Nguyet project can be put into operation in the third quarter of 2020. Notably, VCSC believes that thanks to its abundant financial potential, PVS will enjoy low interest rates (LIBOR + 1.7%) and it is likely that the upcoming FSO / FPSO investment will also enjoy the same interest rate such as FPSO for Nam Du - U Minh project.

According to VCSC, the expansion of capital construction investment will support EPS growth in the coming years. PVS expects to invest VND1.2 trillion in 2019 while this figure is only VND83 billion in 2018.

PVS stock changes from the beginning of the year till now.

PVS expects to pay cash dividend of VND 700 / share (dividend yield of 3%) for 2018 and has been approved by shareholders. The company also expects to pay cash dividends at this level for 2019 but is also willing to propose an increase if the 2019 result is higher than the target.

In 2019, PVS plans to achieve VND 13,000 billion in revenue and VND 700 billion in pre-tax profit, 11.2% and 28.3% lower than 2018, respectively. VCSC believes the company will exceed the set target.

Minh Anh (ttvn.vn)

Tin liên quan